well, duh. Your Bank will just stop allowing you to overdraft, declining your Transactions.

I have never ever had a transaction that overdrafted where I was happy they didn’t just decline it. Zero desire to pay $38 for the “convenience” when I could have just used a different card.

I’ve asked my bank to not allow it on my account at all and they told me NO, they can’t do that, because it’s “a service we provide our customers for their convenience”. Right. I don’t want that convenience, dicks.

No, I want to hear the warped logic.

Then again, it may just be: no income for the banks, they go bust, who will provide banking services to poor people? kind of retarded mental gymnastics.

kind of retarded mental gymnastics.

It’s 2024 you know that’s not cool to say dude

I honestly don’t understand who is supposed to be offended by the r-word. Do people actually identify as that and take offense? shouldn’t they be just as offended by any other term that denotes a lack of intelligence?

It’s 2024 I do not need to explain this. Google it or something.

plaintext

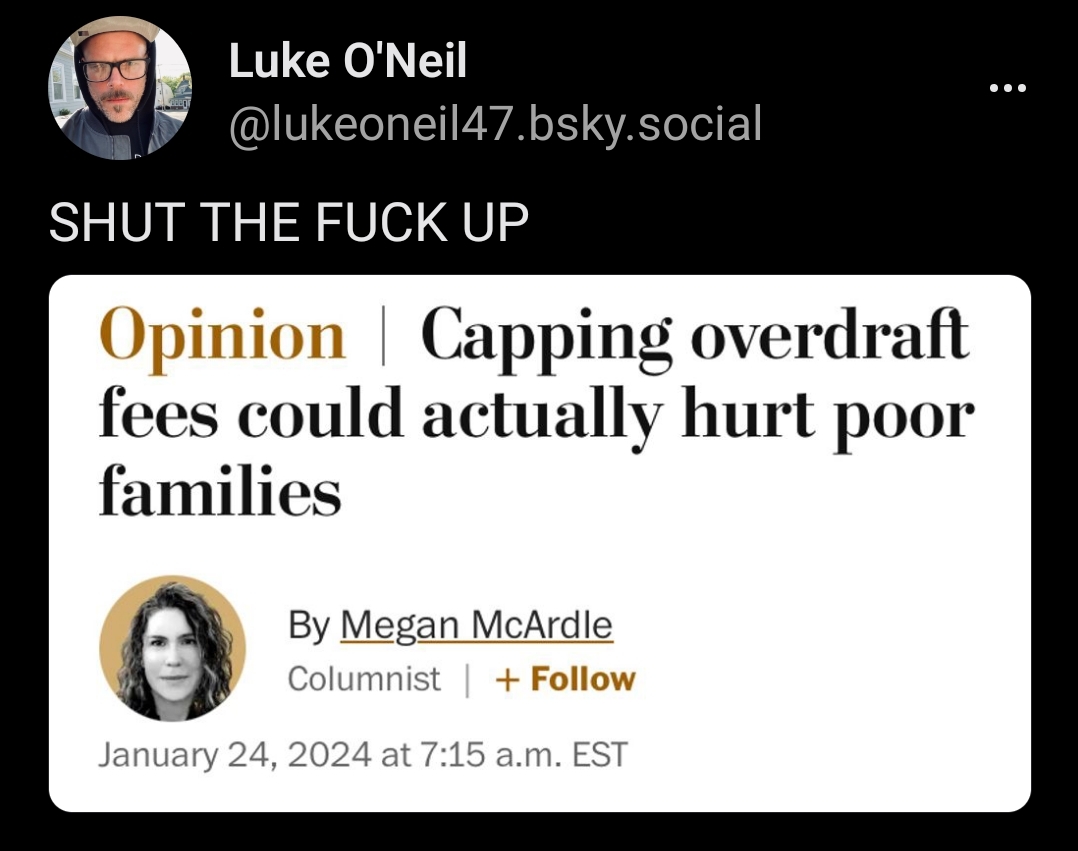

These people are far and away the heaviest users of bank overdrafts. The Financial Health Network, a personal finance nonprofit, says the group most likely to overdraft includes “financially vulnerable” households that struggle to pay their bills every month and typically make less than $30,000 a year. Almost half of financially vulnerable households with checking accounts overdrafted in 2022, and of that group, two-thirds overdrafted at least three times, one-third did so six or more times, and one-fifth overdrafted 10 times or more. With an average overdraft fee of $26.61, hundreds of dollars in fees can land on the most cash-strapped customers. Capping those fees — possibly as low as $3 — would be a huge boon to families who really need the help. Who could oppose that?

Well, as with any nice-sounding policy, it’s important to consider the alternatives, both for the customer and for the banker.

For depositors, overdraft fees can be an expensive alternative to even worse options, such as payday loans or having their electricity shut off (and paying a reconnection fee to turn it back on). And “the best of bad alternatives” can also be sort of true for bankers, who must find some way to defray the cost of providing what is basically an unsecured loan to people who are, as we’ve seen, often financially struggling and might be unable to repay the money. The fees also help pay for “free” checking (which costs banks quite a bit of money to provide).

If we cap overdraft fees, how will banks make up the lost revenue?

From profits, you say, and fair enough, but Patrick McKenzie, who writes the Bits About Money newsletter, points out that the reason your bank is so obsessed with getting you to sign up for paperless statements is that the profit margins on checking accounts are so thin, they can be meaningfully improved by saving the cost of 12 stamps a year. “Margins on small bank accounts are very thin,” he wrote recently, and “credit losses can easily be larger than several years of them.”

Now the government wants to make those accounts even less profitable. It seems possible banks would look to limit their losses by getting rid of those customers or making up the revenue somewhere else — or possibly both. This seems to have happened in the past, judging from what we saw when federal regulators preempted some state fee caps in 2001. According to researchers from the New York Fed, the exempted banks both raised overdraft fees and expanded available overdraft credit, while lowering minimum balance requirements. The rate at which checks were returned for insufficient funds declined by 15 percent. And the share of low-income households with a bank account rose by 10 percent, suggesting that minimum balance requirements had kept those households from opening accounts.

That doesn’t mean that no one would benefit from this rule. High overdraft fees can also deter people from opening a bank account, and it’s possible that effect would outweigh any contraction of credit. The financial industry has also changed a lot since 2001, with nonbank alternatives, such as Cash App, that might offer the marginal bank customer a better replacement than an old-fashioned check-cashing store. But there would still likely be winners and losers, and I don’t know whether the former’s gains would outweigh the latter’s losses. I’m not sure the administration does, either.

Crux of the argument?

Profit margins are very small on small personal bank accounts. If NSF fees are reduced, how ever will we profit from these tiny accounts?!

One bank made only 49 billion profit last year, up from 48 billion in 2022. Why won’t somebody think of the banks!?

Oh no, anyways credit unions exist and rarely have these issues

Credit unions would actually be impacted far more from this legislation than banks.

They don’t have access to the same cash making options that large banks do, and credit unions are also non profit.

If their fee income was reduced, they would have to make up for it in other areas, such as higher lending rates, which affects more people than overdraft fees.

Personally, I’d rather deal with overdraft fees than have a higher rate for loans. If you learn to bank responsibly overdraft fees won’t be an issue anyway.

Overdraft fees simply wouldnt be an issue if they didnt exist. Theres no reason a transaction shouldnt decline if there are insufficient funds. If you dont have the money then you dont have the money.

Theres no reason a transaction shouldnt decline if there are insufficient funds.

I’ll admit I’m ignorant to banking on a large scale, but the few banks I have used and worked for I’ve always had the option to just decline “overdraft protection” so indeed if I tried to make a $50 purchase and I had $45 in my account, it would just decline. Overdrafting has always been an optional service. Are there banks that force you to enable overdrafting?

Edit: now whether the choice is properly conveyed to people is another matter of course, I imagine many banks make it seem like a “good” thing or the default option.

Credit Unions is the answer if anyone actually believed this could even be slightly possible.

The general concern is if you remove the overdraft fee as a tool, banks will just require a minimum or cancel you.

If financially struggling families can’t even access basic banking, they are further disenfranchised and removed from a stability, and eventually wealth generation

Sounds like a great time to actually bring back postal banking if the “job creators” can’t handle just making “some money” instead of " lots of money" from these accounts.

I’m sure the post office would be glad to have the “some money.”

Sounds fine. And unfortunately banks are extremely real job creators. The existence of loaned capital to start business, pay employees and so on are a course of business development.

Ultimately, weather you like them or not, you can’t force a business to work with a given customer, especially if that customer is unreliable or requires more work.

I agree the time of government is to look after people with less/no concern for their profitability, especially when basic well-being and stability are in play.

Well under Obama there was that weird sorta savings account thing they had. I dropped twenty bucks in it just to check it out. They ended the program I think in 2014.

I more assume “banks will stop offering services if they make less” or “those hard limits teach you to not go below 0” which are dumb

Ugh I feel dirty for reading the article but the argument is your first option: “limit bank profits and they’ll stop doing business with poor people.”

Yeah stop talking about corpos like they’re forces of nature or phenomena . “Oh if the bank no money then no loans or whatever” nah that’s a choice. Made by people. People with cars that can be keyed. Allegedly.

Fucking how? What strange form of logic does this idiot use?

I have definitely avoided much bigger late fees via overdraft when I was younger. There’s a middle ground here between predatory fees and getting fucked over a few pennies imo. Let people run a negative balance and then defer the fees if the account goes positive again within a certain timeframe.

Gonna go out on a limb and think it’s something along the lines of: but then the stupid POORS won’t know not to overdraft their account! Nothing will incentivize them to not be poor!

Megan McFuckwit should probably shut the fuck up, the class traitor.

Haven’t heard that term in a while.

If we cap overdraft fees, how will banks make up the lost revenue?

Get in the fucking sea.

Obv the banks can fuck off, but I do seriously worry that we’ll see a response from banks regarding this, and it will probably be an increase in banks requiring your account to hold a minimum balance. They’re both pretty bad, so I’m not sure which is worse, but larger minimum balance requirements could push some people out of reach of a local bank account.

If banks are funded by the government (ongoing bailouts and ridiculously beneficial laws for them) then they should be considered a public service and available to everyone, at least at a basic level

It did in the early 1900s to about late 1960s. It was killed because some banking lobbyist killed it.

Tapping out could be more damaging to child wrestlers’ health than letting 300lb professionals chokehold beyond unconsciousness. Here’s why…

There are definitely scenarios where the ability to temporarily overdraft an account saves people much bigger missed payment fees and interest charges.

I don’t know why we can’t just have the fees come on a deferred basis. Like if your account returns to positive within the billing cycle then the fees get waived. No reason they need to be predatory

I don’t know why we can’t just have the fees come on a deferred basis

The other guy already said it but I’m going to reiterate for emphasis:

Banks are not your friends. Banks (in the US) exist as for-profit businesses to make money off of you

Edit for clarity: The main way banks make money off of you is by investing the actual cash you give them and agreeing to cover your day to day costs of living. Since the vast majority of people prefer to have a positive bank balance and possibly a savings, it works out that the banks always have money to invest.

It stands to reason that anyone with a negative balance is actively infringing their strategy to invest excess money, so why wouldn’t they charge them? It’s all business.

Because I would imagine that the banks don’t want to give a small interest free loan in that scenario? With no collateral on a regular recurring basis that one day will never be paid off?

Not that I feel bad for the banks…

Note: I’ve turned overdraft off with every account I’ve ever used and I don’t use Auto pay because you gotta be strategic sometimes.

Under very, very limited circumstances, maybe. Like you need gas to get to work now, get paid tomorrow, and have nothing in your account? Yeah, maybe, but that’s an expensive tank of gas for someone that’s that short on cash.

OTOH, I can’t count the number of times where my former bank processed my paycheck last–even though it went in first–and then hit me with overdraft fees for buying groceries, gas, paying bills, etc. (This was National City Bank; they ended up losing a class action lawsuit about it, but they still made more money from their theft than they had to pay back out.)

IMO, there should be zero overdraft fees; if the money isn’t in your account, the charge is declined. All of this shit should be done in real-time, instead of waiting for a merchant to post at the end of the day. This is the twenty-fucking-second century, and it’s not that goddamn hard.

Upsetting to hear banks don’t get any better a century from now. Good luck to you future man.

What’s funny is that it looked odd when I read it, but I just quickly brushed it off as a “well you don’t see it written often.”

Or even better, make banks immediately start treating any negative balance as a credit. There can be a low limit, but enforce a low interest rate. For all that banks have done to us, I feel like this is literally the least they can do—and shit, they’d still turn more profit.

Something something most of Europe does not allow you to overdraft your account and people get by just fine something

A lot of US banks also have that as an option, people opt in to “overdraft protection” anyway. The banks make it sound like a safer option, instead of the predatory practice it normally is.

But clearly you guys have less freedom than Americans, because that’s what American TV told me.

The right to be exploited is sacred to us!

people get by just fine

debatable but otherwise the point stands.

Megan is a national treasure.

You can always count on her to selflessly use her to name to publish the most absurdly dog shit arguments to defend corporations and the powerful.

She’s also pretty dumb.

How much are your banking fees? In the UK almost all fees are £12.

Anywhere from $15 to $50+

Wow I wonder what the upper end is. We capped ours at that amount a good while ago now. When I worked at a couple of banks back in 08-14 they weren’t exactly new either.

Here’s some context for you.

For most of my life, banks ran an algorithm on overdrafting accounts so that charges would clear in whatever order triggered overdraft protection the most times. It was an open secret, then it came out and companies tried to insist they could do whatever they wanted.

Lots of real world cases of a single unexpected charge coming in and clearing a full day earlier than expected so a bunch of small charges (a pack of chewing gum) would each trigger the fee. $100 total charges, $500+ in overdraft fees.

Don’t transactions have timestamps? Or are you talking about paper cheques? Like I don’t trust the big banks in my country either, but I’m pretty sure all transactions are logged in real time and can’t be rearranged later.

Again, different countries might have banks work differently. When a debit is being applied (money removed from the account) it has a lifetime. First it is pending, and then it “clears”.

It clears when the bank approves that the money transfer is definitely happening, and that is the moment it is removed from your account. Importantly, the debit clearing from your account on a purchase does not mean the other party has fully received the money.

It used to be that a lot of charges would sit pending overnight and then all pending charges apply in the morning. Yes, even small purchases like a pack of gum bought at the corner store. All they did (and I think Wells Fargo in particular got caught and there were lawsuits about this) was decide the order of clearing pending charges with the intent of maximizing overdraft fees.

And how does that work? Let’s say I have $1000 in my account but forgot my $900 rent is coming out. ALong with some other transactions, they could clear like:

They could $0.99 gum, $150 car payment, $150 groceries, $900 rent. Overdraft fees = 1

Or

$900 rent, $150 car payment, $150 groceries, $0.99 gum. Same transactions processed at the same moment. Overdraft fees = 3! When that stuff happened to me back around '04, overdraft fees were $35 per overdraft. So that example was a $70 difference. In reality, between billpay and small purchases, the difference might be $500+.

My true story was that I had a dick of a landlord. My Bank’s autopay was running slow and despite the bank check already being in the mail and deducted from my account, my landlord insisted I pay immediately, and I was dumb enough to cave. So I cut him a check and asked him to hold it a day or two til the actual check was delivered; he cashed the same day. Double-rent for a 24 year older meant my account went into the red. I had 10 pending transactions (from gas to bill pays) for the next morning. All 10 (despite being already delivered and should’ve cleared first) waited to clear until the double-paid rent cleared. I was charged $350 in overdraft fees, almost as much as my $500 rent was (cheap back then lol). And despite agreeing the check getting to him late was their fault, my bank refused to refund more than $100 in overdraft fees because that’s what their algorithm valued my business at. I got the first rent payment back, fortunately. But was still out $250.

If I recall, the canned defense for this in lawsuits is “we just coincidentally process all transactions large to small instead of old to new because it makes sense to the bank to do so”. If I recall, some states (maybe fed?) ended up having to pass laws regulating overdraft fees a bit. It didn’t go far, but from what I hear it stopped that particular behavior.

This is very sad.

For us the transfer is either near-instantaneous (new system, called UPI) or done in batches every half an hour (old system). I guess this is why banks can’t do this trick.

I think it’s closer to that way now. There was incentive to banks in the past to process it differently.

That said, my bank’s “pay bills” function still takes your cash out before sending the check, despite the check NOT being a cashier’s check when not linked to an e-account. They just refund you in 90 days (or so) if it isn’t cashed.

Megan McArdle is the dumbest bitch in the world. I refuse to click on anything she writes because her shitty takes don’t deserve views. She’s actually a big part of why I unsubscribed from WaPo (that and the whole neolib vibe) because I want zero of my dollars benefiting her.

I have no desire to read but I bet her argument comes down to “if they don’t have overdraft fees then they will go into deeper debt by overdrafting more and that is worse somehow”

All the extra debt they get could have been bank fees, why don’t you think of the starving CEO’s, else they can’t afford their Beluga Caviar and Dom Pérignon dinners.

{kind=link}